Runaway debt and an unfunded pension system make 401K nationalization not only a possibility but a very real likelihood

According to USDebtClock.org the U.S. federal government is more than $19 trillion in the red. That’s more than $59,143 of debt for every man, woman and child.

Within the runaway government spending that got us to where we are today, Social Security is the second largest cost at $894 billion only less than the annual cost of Medicare/Medicaid at $1.0 trillion. Both of these programs are seriously underfunded and will cost the government trillions of dollars.

Once thought an impossibility, 401K nationalization is looking more likely as a tool for both the Federal government and corporations to cover wasteful spending and rampant corruption.

Is 401K nationalization coming and what can you do to protect your retirement investments?

The Government Moves Closer to 401K Nationalization

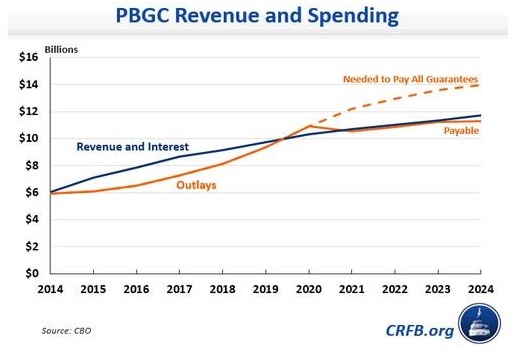

To cover the insurmountable debt, the government has passed a 22% increase in premiums to be paid by employers to the Pension Benefit Guaranty Corporation (PBGC) through 2019. The PBGC was designed to take over bankrupt pension plans and make payments, though payments are normally renegotiated well below what was originally promised by the employer. The new hike costs businesses an extra $14 per employee beyond the 236% increase in per employee costs added by the PBGC since 2005.

Even on the increased premiums to the PBGC, the fund admitted that it was 90% likely to run out of money by 2025.

The combination of building national debt and underfunded needs at both the federal and corporate level means lawmakers and corporate management are going to be scrambling to find money to fill the coming gap.

And that is when 401K nationalization will become a reality.

There are currently about $3.7 trillion saved in 401k plans and other employer-sponsored retirement accounts. Yes, the government knows that we are saving that money to use during retirement, but that didn’t stop them from raiding the Social Security coffers. How long will it be before the government mandates that a certain portion of 401k accounts be invested in government-backed investments like Treasury bonds? After all, just last year the government announced the creation of MyRA plans that are nothing more than bond-based IRAs.

In fact, the Pension Protection Act of 2006 might actually make it easier for 401K nationalizations to become a reality. The law was the beginning of a long list of investor protections that were wiped from the rules, allowing employers to automatically enroll employees and protecting 401K plan sponsors from liability in the event of loss.

What Can Investors do to Protect Themselves from 401K Nationalization?

Protecting your investments from a 401K nationalization or from corporate malfeasance raiding the funds means taking control of your own assets. An investor’s best course is to take control of their retirement investments through the 401K rollover process. A 401K rollover is a relatively easy process where you transfer the assets within your corporate 401K into an Individual Retirement Account (IRA). The IRA benefits from all the same deferred-tax advantages of a 401K and you can make tax deductible contributions every year.

It’s your name on the IRA account and neither the government or an employer has access to it. Learn the differences between 401K vs IRA and critical questions you need to ask. 401K rollover specialists can answer your questions and can help you understand the rollover process to protect your money.

Like and Share this post if you want the government to let you decide how to manage your retirement account funds.

Learn how investors are rolling over their retirement accounts for safety and stability against financial disaster

The 2008 financial crisis affected the lives of people all over the World. Long-standing investments were shattered, jobs were lost, and the systemic collapse of financial markets resulted in immense hardship.

Subsequently, retirement accounts took a major hit. Retirement investors had little to no control over the outcome as Wall Street bankers went gambling with complicated derivatives and other financial alchemy.

But there is a bright side.

People learned from the event. They found ways to take better care of their savings, to protect their retirement accounts from volatility and mismanagement, and decided to take the future of their finances into their own hands.

What did many retirees and future retirees do to protect their nest egg? They rolled over their employer-sponsored retirement plans to individual retirement accounts, and the statistics prove it.

The Great Retirement Account Rollover

According to the 2014 Investment Company Institute (ICI) Fact Book, 49% of traditional IRA-owning households have made rollovers at some point in time. Nearly half of traditional retirement account owners have decided to rollover their funds from employer-sponsored accounts such as 401K and 403B plans.

More telling is the dates behind the retirement account rollover trend.

Between 1990 and 1994, 5% of IRA owners had made a rollover. Between 1995 and 1999, 10% had made a rollover. The number jumps to 29% between 2005 and 2009 and to 34% by the time 2010 rolls around.

Employer-sponsored retirement account rollovers increased 29% (from 5% to 34%) between the early 1990s and the years following the 2008 financial crisis. Why would this happen?

What we find is that individuals viewed that a portion of their losses resulted from the vulnerability and lack of control their funds experienced being under 401K plans, 403B plans, and other types of employer-sponsored retirement accounts.

According to The New York Times, 401K plans and individual retirement accounts lost $2.8 trillion in value in 2008. On average, U.S. workers lost almost a quarter (24.3%) of their 401K accounts. These are retirement accounts that people have been slowly building for years and years, and in one instant, their value plummeted. Part of the reason is due to employer control in the investment of these accounts.

Also in 2008, 72% of workers held 20% or less of their account balances in company stock. However, nearly 7% of 401K investors had more than 80% of their account balance invested in company stock. This exemplifies a mismanagement of those funds, which contributed to glaring losses. Having too much of your retirement account invested in company stock leaves you vulnerable to the company going out of business, getting bought out, or filing for bankruptcy, as what occurred in numerous companies after the financial crisis.

It is clear that investors wanted more control and transparency in terms of their retirement funds. But why choose self-directed IRAs over other investment options?

The Advantages of Rolling Over Retirement Accounts to a Self-Directed IRA

Self-directed IRAs act independently of the ups and downs of one’s employer. Funds in these accounts will not be affected if your company goes out of business, if it gets bought out, or if it files for bankruptcy. Many 401K plans were absorbed or liquidated during the financial crisis. Investors want to protect themselves from the same outcome repeating itself.

The freedom and flexibility of IRA investment options also makes rolling over to a self-directed IRA an attractive option. You have the freedom to invest in real estate, private businesses, and precious metals (a relatively stable investment) which employer-sponsored plans may not support. You also have the option of doing your own research and diversifying your funds to take on the risk only you are willing to.

You are typically free to invest in any or all of the following:

Certificate of Deposits (CD’s)

Bonds

Mutual Funds

Exchange-Traded Funds (ETF)

Stocks

Annuities

Real Estate

Precious Metals

With a 401K, the plan is usually set up by your employer with a large financial institution, limiting your investment options to what the institution offers.

In addition, fees for IRAs are typically lower than that of 401K plans, and your individual retirement account will retain all of the accompanying tax benefits. Stability, lower cost and control are just a few of the advantages in an IRA vs 401k account.

How to Rollover your Retirement Accounts

We advise consulting a tax advisor if you feel that rolling over to a self-directed IRA is right for you. There are many companies that understand the process, know the market, and will be very willing to guide you through the process. With a competent professional, it should not take more than two to three weeks to have your funds fully rolled over into your hands and invested to your liking.

401kRollover.com is dedicated to providing accurate, up-to-date information about 401K rollovers and custodian-to-custodian transfers, so rest assured that we are here to help and guide you to a healthy and vibrant financial future.

Take advantage of a self-directed IRA for more investment options with your orphaned 401k

Job security isn’t what it used to be and few workers stay with one employer for their entire careers. When you leave your employer, what should you do with your orphaned 401k plan (or 403b plan if the employer is a non-profit or governmental entity)? You basically have four options:

Transfer the account into a managed IRA (Individual Retirement Account)

Transfer the account into a self-directed IRA

Roll the account into another employer-sponsored 401k, if one is available

Cash out the account

Cashing out your orphaned 401k accounts is not an option, even if you’d like to use the money. Cashing out a 401k will mean a 10% withdrawal penalty plus paying income taxes on the full amount. Setting the precedent that it’s acceptable to withdraw money from your retirement accounts is going to leave you penniless in retirement.

Rollover orphan 401k Accounts

Rolling your orphaned 401k accounts into those run by a current employer may not be the best decision either. Most employer-sponsored 401k plans offer extremely limited investment options in funds where the manager happens to be offering the biggest fee kickback to the plan administrator. It’s still a good idea to get the full company match on contributions but putting more money to overpriced funds with high commissions won’t help you reach your financial goals.

For most people, rolling their 401k plan into a self-directed IRA is the best alternative. According to Cerulli Associates, a Boston-based research firm, around three million American workers rolled approximately $289 billion from employer plans in 2012. The bulk of this money, or almost $204 billion, was rolled into IRA accounts controlled by financial advisors. Another $85 billion was rolled into self-directed IRA accounts. The company also estimates that by 2017, Americans will roll $451 billion into self-directed IRAs, making this an $8 trillion market place.

Advantages of an IRA vs orphan 401k plans

There are quite a few benefits to an IRA. If you have several orphaned 401k accounts, you can consolidate all of them into one account for ease of management and tracking. Most 401k plans have limited investment options and can charge high management fees to its participants. By rolling orphaned 401k accounts into a self-directed IRA, you gain better control of your retirement investments and the associated expenses. It may also be wise to sever ties with former employers depending upon how you left your job and the financial stability of their retirement plan. With the pension system crumbling, corporate sponsored 401k plans may be an easy target for corporate malfeasance.

There are specific rules governing a 401k rollover which must be followed to avoid withdrawal penalties and taxes. The funds will go into either a Traditional IRA or a Roth IRA depending on when you want to incur the inevitable tax impact. Managed or self-directed IRA accounts also offer different benefits depending on your needs and financial goals.

A managed IRA can offer many more retirement investment options than an orphaned 401k. Alternatives may include stocks, bonds, ETFs, CDs and mutual funds, but this type of account will also be controlled by a financial advisor. This advisor will charge fees and/or commissions for his services.

A self-directed IRA allows for a greater variety of investments such as physical gold, real estate, foreign businesses, horse farms, etc. The options are limited only by the investor’s imagination, risk tolerance and IRS rules and tax laws. This form of IRA truly gives the investor freedom to use his money how he sees fit to best serve his needs. A self-directed IRA also allows for greater financial diversification – for example in physical metals like gold and silver which is very appealing to many US investors today.

Before deciding if a self-directed IRA is best for you, consider how you want your hard-earned money to work for you, the benefits and restrictions of each type of account, and of course the tax implications you may face. Of course you can always contact the orphaned 401k experts at 401krollover.com. Our experts can help you select the best IRA options for your unique needs.

After years of hard work, saving and planning, you have finally reached retirement. Now the most important question on your mind is, “Will my money last for the rest of my life?” In 1994, a financial planner named William Bengen developed one of the most popular rules of retirement spending. The 4% rule of retirement spending caught on quickly and has been quoted by nearly every advisor. The rule has become a safety net for many advisors and their clients and is based upon the following parameters:

Your retirement portfolio is comprised of one-half stocks and one-half bonds.

In the first year of retirement, you calculate 4% of the total account balance. This is the amount of money you can spend within that first year. For example an account balance of $1 million would allow for $40,000 based on the rules of retirement spending.

Every year thereafter, you adjust for inflation and add that adjustment to the original 4% amount. For example a 3% inflation rate would allow for an additional $1,200 of spending in the second year, or a total spend of $41,200.

If you do not spend more than 4%, adjusted for inflation each year, your account will provide a steady stream of funds while also keeping a balance well past your 125th birthday.

A Little History about the Rules of Retirement Spending

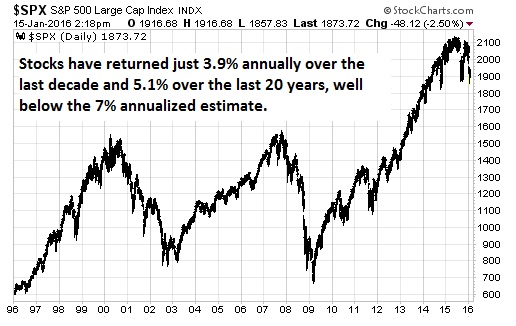

How did Bengen settle on 4% rule of retirement spending as the appropriate annual withdrawal amount? It starts with the unrealistic assumption that stocks and bonds can produce an annualized rate of return of 7%. This figure was based upon information gathered twenty years ago. Since Warren Buffet had predicted that the US stock market will experience a 7% long-term annualized return for the next few decades, we’ll play along, for now.

Next, the rule assumes that inflation will erode the dollar value at the rate of 3% per year. Reducing the 7% annualized rate of return by the 3% rate of inflation leads to an annualized real return of 4%. Bengen then reviewed studies of stock and bond returns dating back to 1926. At that time his retirement spending rule worked in every historical 30-year period, as well as in most computer simulations based on the historical rate of return.

At first, the rule on retirement spending gave many retirees a sense of comfort and security. They just needed to set up a retirement account, save as much money as possible and then set up the 4% rule and forget about it. However, based upon the changing nature of our economy over the past 20 years, the 4% retirement spending rule just doesn’t fit as well anymore and it can’t provide the return most investors crave in today’s economic environment.

What has Changed Since the Rules of Retirement Spending were Suggested

Financial advisors are concerned about multiple factors which have changed in the 20 years since Bengen’s rules of retirement spending were proposed.

Interest rates are so low now, they will almost certainly increase, which will negatively affect stocks and bonds

In 2014 the true rate of inflation, per ShadowStats.org, was 9.4%

The stock market has crashed and rebounded several times making one average forecast inappropriate

Global central banks’ money printing programs could have serious consequences on the rate of inflation going forward

The fact is that the stock market has missed Bengen’s estimated return by a long-shot and multiple market crashes make even the long-term return unlikely. The future return on stocks and bonds is likely to fall well short of expectations, turning the rules of retirement spending upside-down.

So Does the Retirement Spending rule Still Fit Today?

The key to the 4% retirement spending rule is the expected rate of return on stocks and bonds which is required to replace the amount being spent each year. Wade Pfau, professor of retirement income at the American College for Financial Services, argues that asset prices have less room to rise in the future and the long-run outlook calls for lower returns ahead. For example, the 10 year Treasury bond is currently yielding 2.1% as opposed to its historic average yield of 3.5%. Today’s 10-year yield will generally predict the total return expected for the next decade.

Pfau also raises concerns about stock values. According to Robert Shiller, a noted Yale economist, the large companies which are included in the S&P 500 index are currently priced at 25 times their averaged earnings over the past decade. These prices are significantly above the overall historic average of 16 times earnings. When the price to earnings ratio is high, you can expect lower returns over the next 10 years.

As a result, Pfau is predicting that a portfolio consisting of half stocks and half bonds will realize a annual return, after inflation, of only 2.2% over at least the next decade. If Pfau is correct, a retiree following the 4% rules of retirement spending, with an adjustment for inflation, will run out of money 57% of the time.

So what does this mean for the average retiree? It really depends upon your investment and spending strategies. There’s really two options for investors and new rules of retirement spending. You can decrease your spending rate to 3% which will spread your retirement funds out. For a lot of retirees, this isn’t really an option because of low retirement savings. You can also look for higher returns in alternative assets like precious metals. While gold and silver prices have languished for several years, key factors are coming together that may increase demand just as supply is shrinking. Investing just 20% of your retirement accounts in precious metals could increase your long-term return by several percentage points.

Because of the changes we have seen in the past 20 years, most advisors agree that the 4% retirement spending rule should be nothing more than a starting point for discussions about spending after retirement, and preservation of assets during retirement, to ensure continued financial freedom.

Steps to Take Beyond the Simple 4% Rule of Retirement Spending

Here are some better retirement suggestions to follow:

Save more money before retirement. This sounds obvious, but for many reasons, it is not always possible. With high unemployment rates, increasing medical expenses, and increased costs of living, today’s U.S. citizens are just not able to set aside as much as they want for retirement. More Americans are expecting to work longer than their parents did before they will be able to retire. Save more money by saving on taxes, taking advantage of deductions for retirement accounts and 401k tax breaks.

Be flexible during retirement – both in investing and spending. Reevaluate your financial situation frequently throughout your retirement years. Adjust spending annually, if necessary. Pay attention to the markets when deciding if you can afford that new car this year, or if you would be better served to wait a while. Match your spending and life experiences with your investment performance.

Diversify. Do not just invest in large-cap stocks and bonds. If you invest in assets other than stocks and bonds, you can realize a greater spending potential since your withdrawals are not solely dependent upon market fluctuations and inflation or interest rates. Understand your IRA investment options and the flexibility you have for investing with an IRA transfer from old 401k accounts.

According to John Halloran of Certified Gold Exchange, “Even though interest rates are almost zero today, they are poised to rise for the next 20 years. With government liabilities increasing, you can bet Uncle Sam will try to spend its way out of debt. This uncontrolled spending will really affect the purchase power of many hard-working Americans. Investing in safe havens like gold and silver really debunk the 50% stock 50% bond recommendation which is the basis of the outdated 4% retirement spending rule.”

The best rule today may be to not follow rules of retirement spending at all. Retirees need to be active participants in the management of their retirement savings and adjust spending where needed. Consider a 4% spending cap, but remain open to modification and diversification in order to ensure the comfortable retirement you have worked so hard to enjoy. Let our experts at 401krollover.com help you make the best decisions for your particular needs. Contact us through our website at www.401krollover.com for your own personalized plan.

Use these points to decide your 401k asset allocation and where to put your 401k money

The old rule for investing and asset allocation used to be to subtract your age from 100 for the percentage of your portfolio you should keep in stocks, putting the rest in bonds. The misguided advice has caused millions to miss their retirement goals and misallocate their 401k money.

Besides the fact that Americans are living longer, making the 100 rule obsolete, the rule is an oversimplification that misses out on some very important points.

How Much Do you Need and at What Risk?

A better start to retirement planning begins with an estimate of how much you will need in retirement. You don’t have to be accurate down to the penny but should try to estimate your living expenses to the nearest $50,000 or so. Take your current expenses, deducting those that you won’t have in retirement like education and retirement savings, and then add in new expenses for things like travel. The Department of Labor Consumer Expenditure survey can help you see how much people spend on average according to their age.

Any retirement calculator will show you the return needed on your investments to meet your future spending needs; given things like age, annual savings and current investments. Your next step is to do a reality check on this number.

If you need a return of more than 10% annually on your investments to meet your retirement goals, you may need to rethink your savings rate or your goals. Aiming for such a high annual rate will force you into riskier investments and may cause you to panic-sell when the markets tumble. A return of between 4% and 6% for a blended portfolio of different assets is a more realistic goal.

Your own tolerance for risk will also play a part in your 401k investing plan. There’s nothing wrong with being a conservative investor, preferring stability to the possibility of higher returns. The biggest mistake you could make is chasing returns to the point that market volatility makes you nervous and leads you to commit bad investing behaviors.

Best Investments for your 401k Money

The most ridiculous and overused cliché in the world has got to be, “Don’t put all your eggs in one basket.” Why wouldn’t you put all your eggs in one basket? Are you going to put one egg in a basket and make several trips?

Alas, the intent of the saying is still one of the best pieces of investing advice even if the analogy doesn’t quite work. You need to diversify your 401k investments across several different asset classes and within each asset class or risk putting your retirement in jeopardy.

Stocks are the naïve favorite of 401k plans, mostly because they get the most attention from the media and from advisors. Be wary of your 401k advisor and their recommendation for stock funds. These funds normally charge a higher management fee and the advisor may be getting a bigger commission to recommend them. Since you are more limited to your investment choices in most 401k plans and stock funds carry higher fees, it might be smarter to hold less stocks in your 401k compared to other assets. You can carry a larger weight to stocks in your self-directed IRA accounts or other investing accounts to balance out your portfolio while benefitting from the widest selection of investments.

Bonds and bond funds are also a popular 401k allocation choice but you might have more invested than you think. Advisors have been pushing target-date funds recently, mostly because they pay higher fees, and many of these carry large weightings in bonds. There is nothing wrong with holding a large percentage of your portfolio in bonds, it’s absolutely necessary for older investors, but make sure you know how much you have invested across all your bond- and target-date funds.

Precious Metals are an essential but too often neglected component of 401k and retirement investing. Investments in gold and silver have lost favor with investors since the frenzied prices of 2011 but still serve a critical importance to retirement plans. Precious metals provide one of the few real protections in a market dominated by financial assets. Unlike financial assets like stocks and bonds, precious metals are real assets that keep their value against inflation and will increase in value during periods of high market volatility. Beyond the fundamental need for safety, supply and demand are at turning points which may drive prices higher soon and make for very strong investment returns.

Even an allocation to riskier alternative investments like futures and private equity might have a place in your 401k plan. These investments may be higher risk by themselves but will still help to smooth the risk in an overall portfolio when combined with stocks, bonds and metals. You probably don’t want more than 5% or 10% of your 401k allocated to alternative investments but some allocation is important.

Will my 401k Investments Change as I get Older?

Probably the most important thing to remember about your 401k allocation is that it will change as you get older. That stock-heavy portfolio might be Ok for the new investor in their 20s but it will mean way too much risk for the 30- or 40-something investor.

There’s no rule to when you should shift your 401k allocations but most people revisit their strategy every ten years. This makes it easy to remember and avoids changing your allocation too often and paying too much in fees.

Don’t forget that your 401k allocation strategy should be as a part of your entire wealth strategy. It may be a separate account but your 401k money is still a part of your larger financial picture. If you have a large percentage of your regular investing account in risky assets, you might want to overweight your 401k investments to safer assets like bonds and precious metals. This will even out the risk in your overall wealth and prevent a market correction from wiping everything out.

Be sure to rollover those old 401k accounts from previous employers into individual retirement accounts for better flexibility and lower fees.

The Center for Retirement Research has found that 21% of employees who are eligible for a 401k plan at work decline to take advantage of the offer, despite the fact that many employers will match at least a portion of employees’ contributions.

If you’re part of the 79% of employees who see the value in saving with a 401k savings plan, Like and Share this post.

A CPA and IRA consultant from New York uncovered a proposal in President Obama’s 2016 budget plan that would severely limit investors’ ability to save using company 401k plans as well as Roth IRAs. Current laws allow savers to make after-tax contributions to Traditional IRA plans and then convert those Traditional IRAs into Roth IRAs.

Additionally, Obama’s proposed budget would eliminate investors’ ability to contribute after-tax dollars to their maxed-out 401k plans and then convert those plans to Roth IRAs upon retirement.

If you are like the millions of other 401k and IRA owners who plan to use your hard-earned savings in retirement or for your children, Like and Share this post so this budget proposal gets eliminated instead of our ability to save.

President Obama’s proposed budget for fiscal year 2016 includes measures that would increase the capital gains tax on profitable investments to 28%. Obama also wants to put a cap on tax-advantaged retirement accounts like 401k and IRA plans. What’s more, he wants to introduce the Buffett Rule, which requires a 30% minimum federal tax rate for wealthy Americans.

If you believe individuals who save for retirement should be rewarded instead of punished, Like and Share this post today. Together, we can make a difference.

Why have 401k rollovers become so popular over the last few years? Well, since the 1980’s we have been blessed with retirement savings options that take into account our job flexibility and, thus portability. Gone are the days of 40 years with one company, getting a monthly pension and a gold watch upon reaching age 65. Americans have been able to accumulate over $5 trillion in defined contribution plans (profit sharing and 401k plans) according to the Investment Company Institute (“ICI”.) According to Fidelity Investments, the average 401k account balance in approximately $91,000 while the average IRA balance is approximately $92,000. However, the ICI has data that shows the average account balance of the “near retiree” (age 60 to 64) to be approximately $360,000. For many of us, the 401k plan is our largest asset, with the possible exception of our home equity.

So, what makes the 401k rollover so popular? One simple word: CONTROL. When we are in the company sponsored 401k, our investment options are limited. In many cases, the employer contribution to OUR retirement plan is in the stock of the company. You are given the option of investing in a menu of mutual funds or other investment products as selected by your employer. They must uphold their fiduciary duty and, consequently, end up limiting your choices. Better to be safe than sorry, so they think.

When you separate from service with the employer (i.e., quit, laid off, retire) you have the ability to take a distribution from the 401k plan of your entire account balance. This is what is known as a 401k rollover. You can have a check issued to you (be careful) or have a “direct rollover” into an IRA. If the 401k plan is handled by a large company like Fidelity, Schwab or Vanguard, they want you to set up an IRA with them. That may be an excellent move because it is simple and you may be able to keep your investment program intact. However, you have plenty of options. Remember, once you execute the 401k rollover YOU ARE IN CONTROL. You can probably find an investment adviser or a boutique trust company that would love to invest your ½ million dollars!

If you have taken the check for your 401k account balance you have 60 days in which to put it into an IRA rollover account. Otherwise, the amount you received will be treated as income and you will have to pay income tax on that amount. That can be very painful if you are unprepared.

It is highly recommended that you consolidate all of your employer sponsored retirement assets into one account. It is easier to manage and maintain one large account rather than several smaller accounts. You can have all of your previous 401k or profit sharing plans transferred directly into your new IRA rollover account. But do not commingle your regular IRA accounts with the monies from employer sponsored retirement plans. (More on that in a later blog.)

In summary, take full advantage of the retirement programs offered by your employer. Be sure to maximize the company match of your 401k salary deferral. When you leave the company, take the 401k account and put it into an IRA. Now, you are in CONTROL. Your options are virtually limitless and we can tell you more. Even if you do not possess the will, skill or time to invest this significant asset, there are many ways that are available to you. And, remember that this is the source of your retirement paycheck. You earned it!