There may come a time when you need the money that is in your 401k even though you have not yet reached retirement age. You may qualify for a 401k withdrawal if you meet specific conditions but it is critical that you understand rules around 401k withdrawals. When you make a 401k withdrawal, you will have to pay steep 401k withdrawal penalties and 401k taxes on the money that you withdraw.

Eligible Reasons for a 401k Withdrawal

The rules around a 401k withdrawal are set up to help protect your retirement money, so it’s available to you when you retire. If you don’t meet the basic qualifications for a 401k withdrawal, you will not be able to withdraw the money without paying taxes and a penalty. The exemption to 401k withdrawals are considered hardship withdrawals. Each individual plan will have its own criteria for what it constitutes as a being eligible for a 401k withdrawal. These are some common reasons, but not every plan may allow them.

Medical Expenses: Certain medical expenses may qualify for an early 401k withdrawal.

Purchasing a Home: 401k withdrawals are allowed for the down payment on your first home.

Avoiding Foreclosure: If you are facing foreclosure on your home, you can access the funds in your 401k to prevent it from happening.

Other Extenuating Circumstances: An early 401k withdrawal may be allowed for other things such as emergency repairs on your home or to cover the cost of a funeral.

Types of 401k Withdrawals

There are two basic types of 401k withdrawals. A voluntary withdrawal is one that you take out for one of the hardship reasons. You may also face a mandatory 401k withdrawal such as to begin receiving minimum payments once you are 70 1/2 years of age. You may also face a mandatory withdrawal if the 401k administrator determines that you don’t have enough in the 401k account to keep it active. If this is the case, you can avoid the fees and penalties on 401k withdrawals by rolling it into an IRA within 60 days.

401k Withdrawal Limits

When you make a withdrawal from your 401k, you are only allowed to withdraw your voluntary contributions as part of your withdrawal. The amount you earned in interest and the matching amount that your employer has contributed may not be available to you. However, a 401k withdrawal for IRA transfers are completely allowed and you will be able to move the entire amount according to IRA transfer rules. Some of the plans may allow you to access matching contributions as well, but not all plans have such a feature.

Applying for a 401k Withdrawal

In order to make a 401k withdrawal, you will need to prove that you are facing a financial hardship that matches the allowable reasons in your 401k. You can speak to your plan’s administrator to learn what documentation you will need to provide to prove the hardship. As you complete the application, you need to be sure that you calculate the amount you need to include the money that will be sent to the IRS to cover your taxes and penalty. Most plans will send 20% of your total 401k withdrawal.

Taxes and Penalties on a 401k Withdrawal

You will be taxed on the money that you withdraw from a traditional 401k. A 401k withdrawal is taxed at your current income tax rate. This means that if you are in the 15% bracket, you will be taxed at the rate of 15% when you file your return for that year. The 401k withdrawal is counted as income, and it could possibly bump you into a higher tax bracket. You may want to consult with an accountant when you make the withdrawal, so that you set aside the correct amount to cover the taxes that you will have to pay. You should receive a 1099-R form from the 401k plan that reports how much you withdrew, and you will need the 1099-R form handy when you file your taxes.

When you take an early 401k withdrawal, you will need to pay a 10% penalty on your withdrawal. The plan will send that amount to the IRS. You should be prepared to pay this amount. It may make it more difficult to get the amount that you need to cover your expenses.

Alternatives to a 401k Withdrawal

There are alternatives to taking a 401k withdrawal. It’s best if you can avoid taking a withdrawal but there are options that will help save you money in taxes and penalties. One option is take out a 401k loan. This allows you to access the money in your 401k without a 401k withdrawal, and it gives you the benefit of paying the interest on your loan to yourself. There are drawbacks to taking out a 401k loan. You can only borrow from the 401k with your current employer. If you change jobs or are laid off, the entire loan is due in full, or you will be charged the penalties and taxes for an early withdrawal. Just like with a 401k withdrawal, there are limits on the amount that you can take out each year and the reasons that you are allowed to borrow the money.

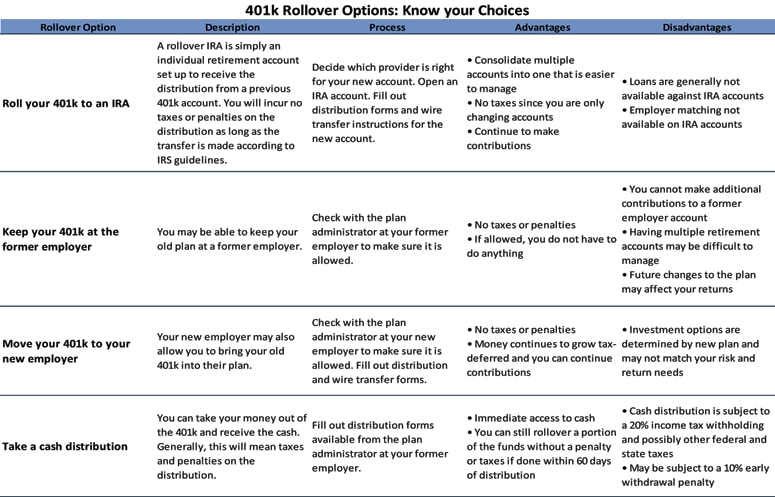

Another alternative to the 401k withdrawal is to roll the money over into an IRA. This only works if you are being forced to do a withdrawal because you do not have enough invested in the plan. You may also want to consider a rollover if you have several 401k accounts through different companies or if you want to have more control over your investments. A self-directed IRA even allows you to invest in property or gold as part of the IRA. You can learn more about the IRA options near you by contacting us.